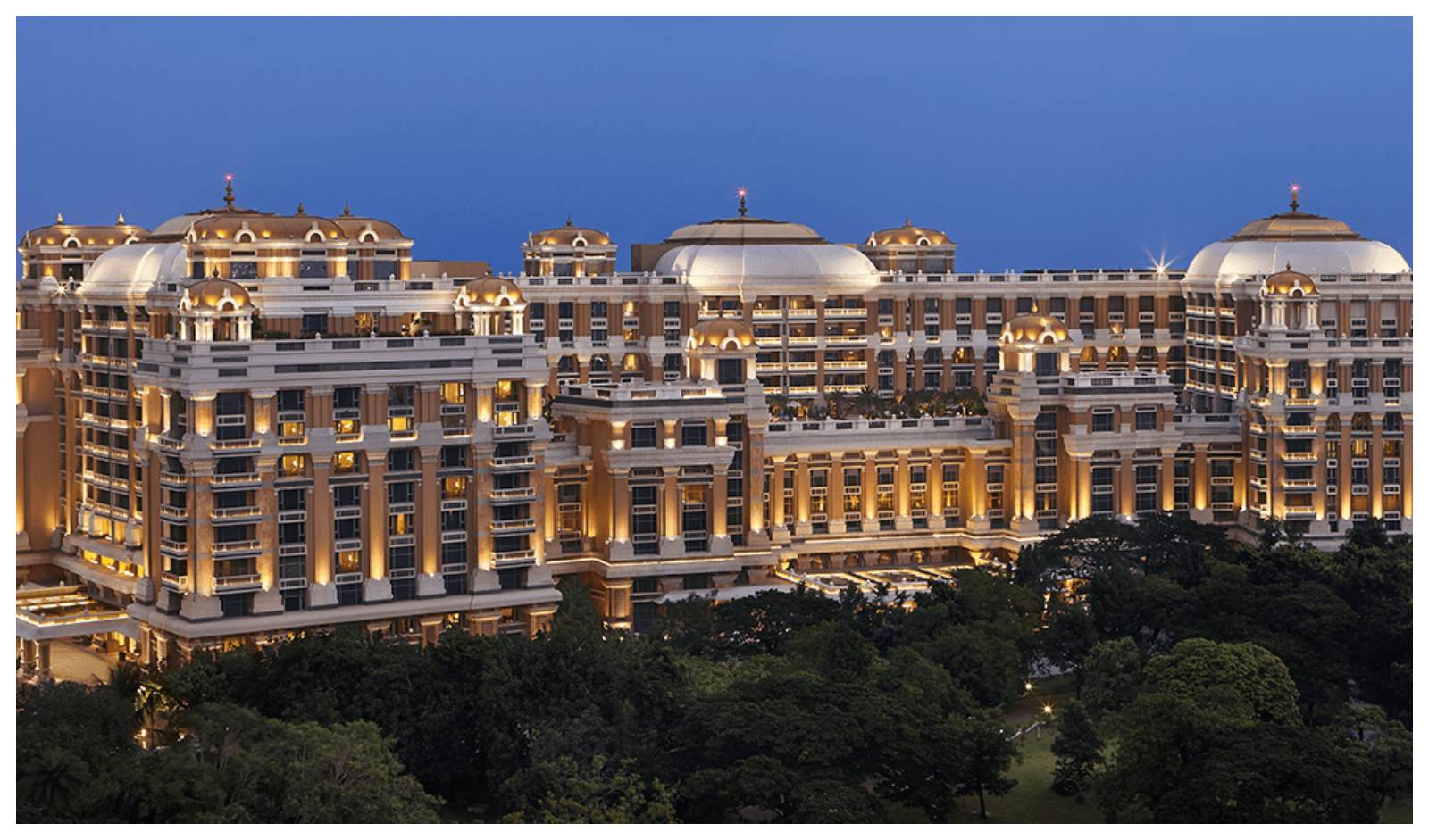

ICICI Securities has initiated coverage on ITC Hotels Ltd. with a ‘Buy’ rating, highlighting strong growth prospects driven by the company’s asset-right expansion model, new hotel additions and rising operating leverage. The brokerage has set a target price of ₹250, implying a 21% upside from Friday’s closing price. It noted that ITC Hotels’ net cash balance of nearly ₹1,700 crore (as of March 2025) gives the company significant room to fund future expansion.

ITC Hotels plans to grow its portfolio from 13,600 operational keys (September 2025) to over 20,000 keys by 2030. ICICI Securities expects RevPAR to grow at 9% CAGR over FY25–28, while management fees are projected to rise at 17% CAGR, supported by a strong pipeline of new openings. Consolidated revenue is forecast to grow at 12% CAGR, and Ebitda at 15% CAGR, with margins expanding by 300 basis points to 37% by FY28.

The brokerage said ITC Hotels' asset-right strategy, adopted in 2018, positions the company for scalable and capital-efficient growth. A pipeline of 59 managed hotels with roughly 5,500 keys, along with greenfield projects and hotels opened since FY20, is expected to drive performance.

Three new projects are currently under development: Puri – 118 keys (Epiq Collection), Bhubaneshwar – 100+ keys (Welcomhotel) andVisakhapatnam – 200 keys. The Odisha hotels are expected to open in FY28, while the Vizag property is slated for FY30, with total capex estimated at ₹800–900 crore.

ICICI Securities flagged potential risks, including slower-than-expected growth in occupancy or room rates and delays in project timelines.

Restaurants in IndiaThe new outlet introduces a refreshed SALT 2.0 experience, featuring a modern, fine-dining ambience, updated flavours and a polished yet warm service…

Restaurants in IndiaThe new outlet introduces a refreshed SALT 2.0 experience, featuring a modern, fine-dining ambience, updated flavours and a polished yet warm service… Food Delivery BusinessThe deal was executed at a 0.7% discount to Friday’s closing price of ₹292.4. Following the transaction, Eternal’s stock erased early gains and was…

Food Delivery BusinessThe deal was executed at a 0.7% discount to Friday’s closing price of ₹292.4. Following the transaction, Eternal’s stock erased early gains and was…-

Hotels in IndiaThe brokerage has set a target price of ₹250, implying a 21% upside from Friday’s closing price. It noted that ITC Hotels’ net cash balance of nearly…

New launchPositioned as Mumbai’s first dedicated aperitivo bar, Call Me Sofia opens at dusk, offering an intimate, semi-open space designed to feel like a…

New launchPositioned as Mumbai’s first dedicated aperitivo bar, Call Me Sofia opens at dusk, offering an intimate, semi-open space designed to feel like a…

Copyright © 2009 - 2025 Restaurant India.